Mobile App

Employees can manage their account and savings on the go with the Vestwell mobile app. They can set contributions, adjust account details, and track progress anytime, anywhere.

Download on the App Store

Government-facilitated retirement savings programs require employers to offer retirement benefits at no cost to them. Help your clients know what is expected.

You can help your clients determine if sponsoring their own plan or facilitating a state plan better suits their business needs. There are three main requirements for employers in state programs.

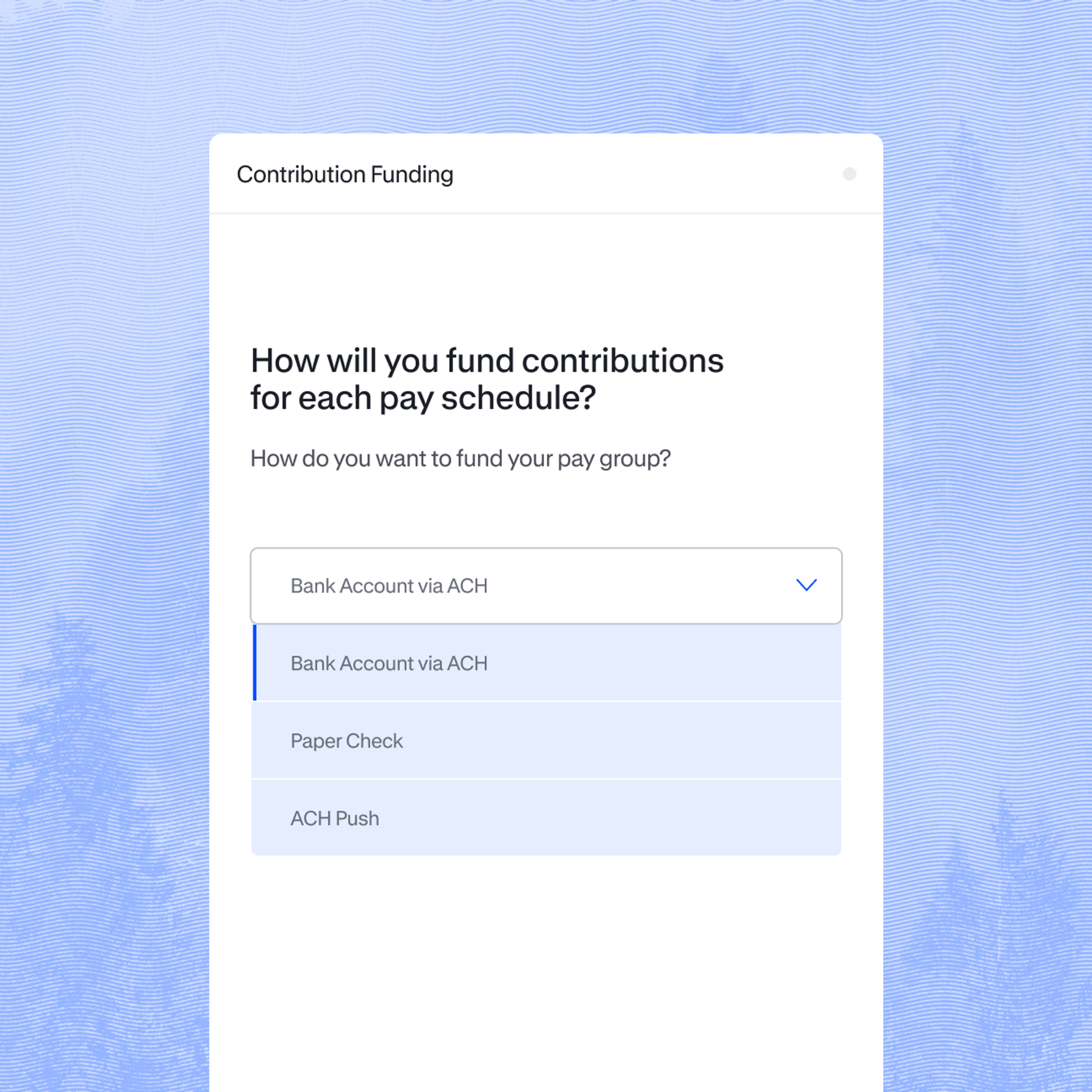

Set up an ID and password, answer questions about the company and payroll process, complete payment setup, and then add employees. A payroll representative can even help facilitate this process.

Once employees are added, we will communicate directly with them to explain their options during the 30 days they have to opt out or customize their account. At the end of the 30-day period, we will notify employers of their choices and send a reminder to begin payroll deductions, and submit contribution information and funding for the employees who choose to stay in the program.

To stay in compliance, employers must continue to send payroll contributions and maintain employee records, including updating contribution rate changes when needed, adding new employees, and marking former employees as terminated.

Employees can manage their account and savings on the go with the Vestwell mobile app. They can set contributions, adjust account details, and track progress anytime, anywhere.

Download on the App Store

Government-facilitiated retirement savings programs require employers to facilitate the program if they have a certain number of employees, have been in business for a specific amount of time, and do not currently offer a qualified retirement plan. These eligibility requirements vary by state. Use our helpful online resource to determine the state mandates for your clients.

A qualified, employer-sponsored retirement plan includes a plan qualified under Internal Revenue Code sections 401(a) (including a 401(k) plan), qualified annuity plan under section 403(a), tax-sheltered annuity plan under section 403(b), Simplified Employee Pension plan under section 408(k), a SIMPLE IRA plan under section 408(p), or governmental deferred compensation plan under section 457(b). It does not include payroll deduction IRAs.

You can easily learn about the developments for a retirement program, possible mandates, and timelines by using our interactive resource online.