The $37,000 Gap: Why Queer Workers Retire With a Third of What Their Peers Have

$14,000 versus $51,000. That's the median retirement savings for an LGBTQ+ worker compared to a non-LGBTQ+ worker.

LGBTQ+ workers aren't saving less because they care less about their future, or because they're earning less interest. They’re saving less because the systems built around them, from wages to debt, benefits, and employment stability, have been quietly working against them for a long time.

This Pride Month, we’re examining this savings gap to understand what's driving it and share what employers can do to help close it.

The Story the Numbers Tell

Starting with savings overall, more than half of LGBTQ+ Americans have less than $5,000 saved, and one in five has nothing at all. On top of that, roughly 65% of LGBTQ+ Americans live paycheck to paycheck, and that number rises to 72% for Black LGBTQ+ Americans. When most of a paycheck is spoken for the moment it hits, the ability to save for the long-term can quickly become out of reach.

The income and earning potential for LGBTQ+ workers play a significant role in the gaps they face. LGBTQ+ households earn just 85 cents on the dollar compared to non-LGBTQ+ households. For transgender and nonbinary households, it drops to 70 cents.

Less income ultimately means fewer dollars reaching retirement accounts. More than half of middle-income LGBTQ+ Americans aren't confident they'll have enough to live comfortably in retirement, compared to just 29% of non-LGBTQ+ Americans in the same income bracket, and 53% of LGBTQ+ workers worry they'll never be able to retire at all.

Read together, LGBTQ+ workers are earning less, saving less, and worrying more, across every category of financial security we typically measure.

What’s Driving the Gap?

Less Access to Workplace Savings Benefits

Only 36% of LGBTQ+ workers have a retirement account, compared to 51% of U.S. workers. LGBTQ+ workers are over-represented in industries with weaker benefits infrastructure, such as service, gig work, freelance, and smaller businesses, which means access itself is part of the problem.

There's also a retention factor. One in three LGBTQ+ employees has left a job because of how they were treated based on their sexual orientation or gender identity. Every job change is a potential break in retirement plan continuity, for example, a vesting cliff that doesn't get crossed, resulting in a few years of employer match left on the table.

A Wage Gap That Starts Early and Continues to Compound

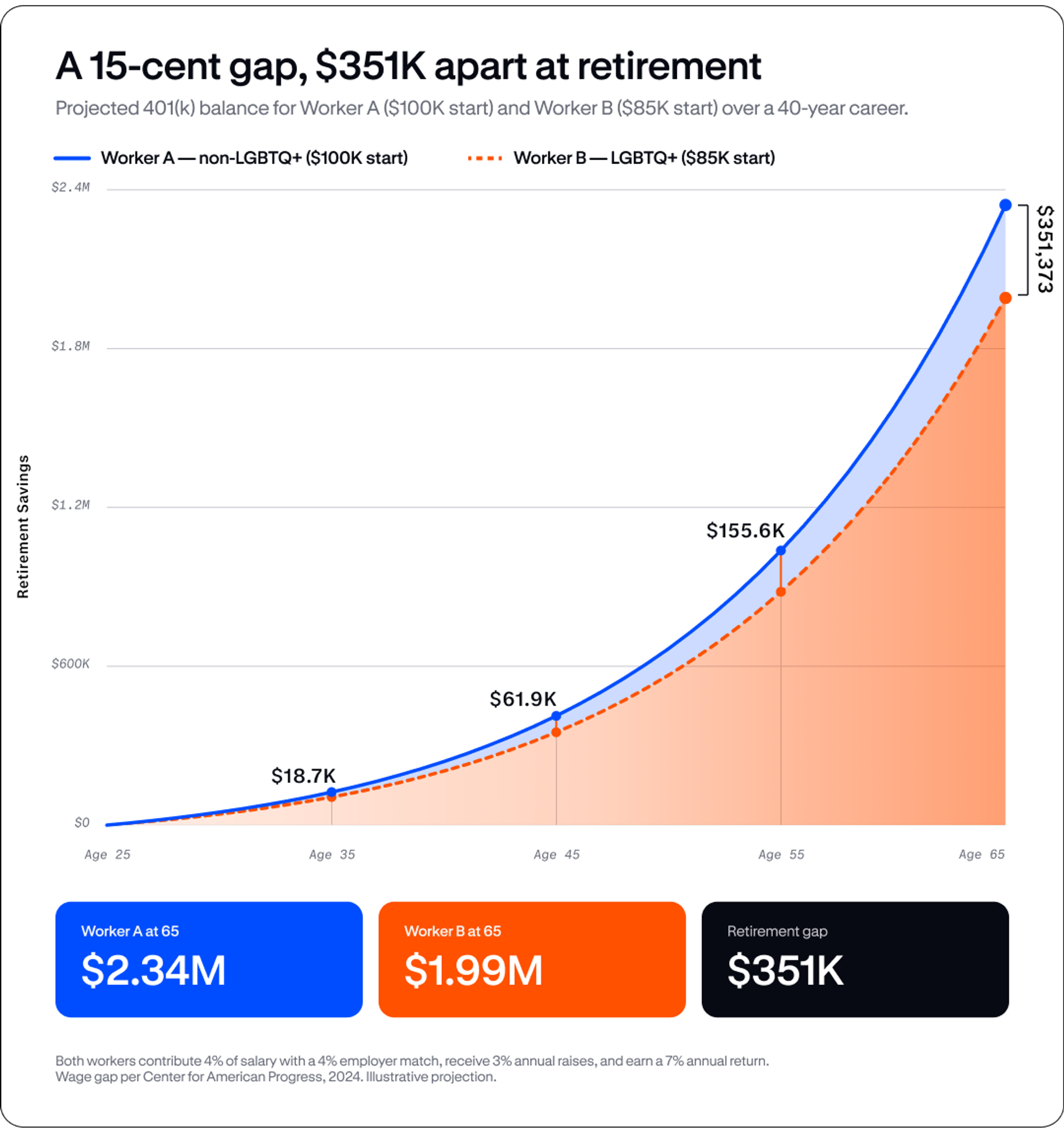

When workers earn less, they save less, and that gap widens over time. A 15-cent shortfall on the dollar in a worker’s twenties may become tens of thousands of dollars in foregone retirement contributions when employer match and compound growth are factored in.

Here's an example of two workers in the same role, broken down. Worker A, a non-LGBTQ+ employee, earns $100,000 a year. Worker B, an LGBTQ+ employee, earns $85,000, representing the 85-cents-on-the-dollar gap. Both contribute 4% of their salary to a 401(k), both receive a 4% employer match, both get a 3% raise every year, and both invest in a portfolio earning a 7% annual return.

Forty years later, Worker A retires with about $2.34 million. Worker B retires with about $1.99 million. That's a difference of roughly $350,000, created by a 15-cent gap alone.

This example highlights one of the most optimistic versions. It assumes both workers have equal access to a 401(k), stay in their jobs for a full 40 years, and never have to pause contributions to cover an unexpected expense. In reality, as explored above, LGBTQ+ workers are more likely to work in industries without retirement benefits in the first place, more likely to leave jobs because of how they're treated, and more likely to pull from savings under financial strain.

In addition, the 85-cent figure is also the most favorable one. For workers carrying more than one marginalized identity, the disparity widens even further. Transgender women earn 60 cents on the dollar compared to the typical worker. Black LGBTQ+ workers earn 80 cents. And LGBTQ+ Native American workers earn 70 cents.

How Employers Can Support LGBTQ+ Team Members

Employers may not realize they can make a significant dent in these gaps through their employee benefits. They just need to be designed to actually work for the people the gap affects most. Here's where employers can start:

Offer a 401(k) with automatic enrollment. Automatic enrollment dramatically increases 401(k) plan participation across every demographic. If you already have a retirement plan, consider adding automatic enrollment and escalation. New plans launched after 2024 are required to include automatic enrollment to help more workers save.

Match contributions. An employer match is one of the best ways to encourage workers to participate in their plan. But it also actively helps employees save more and helps businesses retain talent.

Add an Emergency Savings Account (ESA). 65% of LGBTQ+ workers live paycheck to paycheck, which can make building a savings fund difficult. By offering an ESA, employers can help these employees build a cushion for life’s unexpected moments while also safeguarding long-term retirement savings accounts.

Make the plan accessible to part-time workers. LGBTQ+ workers are more likely to have income from multiple sources. Plans designed only for full-time employees miss a large share of the workforce that needs savings infrastructure most.

Closing the Gap Starts at Work

Workplace retirement plans are one of the most powerful wealth-building tools in the American economy. For LGBTQ+ workers, who face a steeper climb in nearly every category of financial life, equitable access to that infrastructure is a measurable lever for closing a gap that's been widening for decades.

Pride Month is a moment for symbols, recognition, and celebration. The eleven months that follow are the moments for action.

If you're an employer ready to offer a 401(k), expand the one you already have, or rebuild your benefits customized to your team’s needs, Vestwell can help. Vestwell’s modern, flexible workplace savings infrastructure is designed for businesses of every size and built so that everyone you employ can save with confidence.