401(k) Basics: A Starter Guide to Understanding Your Retirement Plan

Although they may seem similar at first glance, your 401(k) is very different from a traditional savings account. Between rules dictating how much money can be contributed to the plan and the differences between a Roth and a traditional retirement plan account, understanding your 401(k) plan can understandably be confusing at times. Below is a quick Q&A of some of the most common inquiries we get from savers just like you.

What are the differences between a traditional and a Roth 401(k)?

The main distinction is the tax benefit.

- Traditional 401(k) contributions are made on a pre-tax basis and individuals pay income tax on the amounts withdrawn once they retire.

- A Roth 401(k) feature allows for the contribution of after-tax dollars. The elected amount is deducted from your paycheck after income, Social Security, and other applicable taxes are withheld.

How does money get deposited to my 401(k) plan?

After you meet your plan’s eligibility rules, there are two main ways that money gets contributed into your account:

- Via your paycheck - Once you have selected the amount you would like to contribute to your 401(k) account, that percentage or dollar amount is deducted from your paycheck. Contributions are set up through your employer’s payroll system and are deducted from each paycheck during the payroll period.

- Via your employer’s contributions - Some plans have something called an “employer match,” which means the employer will contribute to your account based on how much you contribute, up to certain limits established by the IRS or your plan document. For example, if your plan has a match up to 4% and you are contributing 3%, your employer also contributes 3%. If you are contributing 5%, your employer will contribute 4%.

What are the contribution limits for a 401(k)?

It depends.

- For 2026, the limit to contribute to a 401(k) annually is $24,500 (indexed each year for inflation) regardless of whether the funds are a pre-tax or Roth contribution (up from $23,500 in 2025). However, savers age 50 years or older may contribute up to $32,500 annually, and savers age 60 to 63 may contribute up to $35,750.

- $24,500 is the limit you can contribute from your own paycheck. If your plan offers an employer match, the overall limit on contributions made to employees' account cannot exceed the lesser of:

- 100% of the participant's compensation, or

- $72,000

How much should I contribute to my 401(k)?

It differs depending on your personal financial situation.

- This is a decision solely for you to make based on your other investments, your risk tolerance, how much income you think you will need during retirement, and many other factors.

- There are several tools that can help you. Consider using a 401(k) calculator by selecting one of the several options available online.

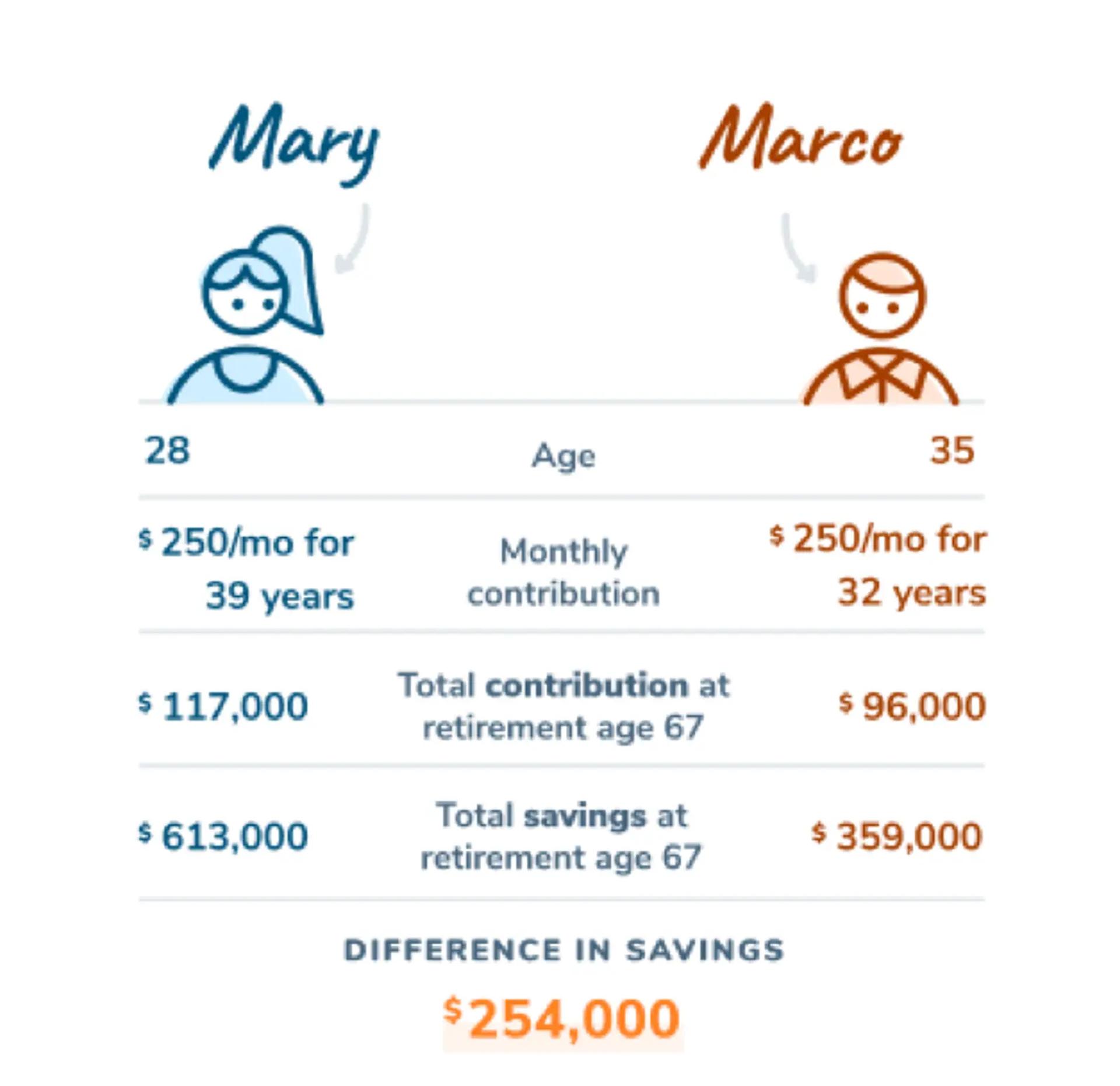

- The most important thing you can do is start saving now. The impact of growth over time can make a huge impact on your accumulated savings due to compounding interest, dividends, capital gains, and investment returns. As an example, Mary saves $250/month starting at 28 years old and Marco saves $250/month starting at 35.* Assuming an annual tax-deferred rate of return of 7.00% compounded monthly, both Mary and Marco retire at age 67 and the difference in their savings is $254,000** despite having only a $21,000 difference in total 401(k) contributions.

What is a rollover contribution?

A rollover contribution is funded from your retirement plan account with a previous employer or an Individual Retirement Account (IRA).

- A rollover contribution refers to the funds that you have moved from your previous employer’s retirement account or another qualified plan into your new employer’s retirement account. If your plan accepts rollover funds, you can consolidate your retirement accounts by transferring assets from those other accounts. For example, if you previously had funds left at a retirement account with ABC Retirement and have started a new job with an employer who has an account with XYZ Retirement, the movement of those funds from the previous provider to the current provider is referred to as the “rollover contribution.”

What are the different ways to withdraw funds from my 401(k) account?

There are a few different ways to get money out of your account depending on the features offered by your plan.

- First, know the basics.

- Your 401(k) is intended to be used after you reach retirement age. To discourage the early withdrawal of retirement plan funds, withdrawals before you reach age 59 ½ are subject to tax withholdings and early withdrawal penalties. Savers are also required to start taking withdrawals when they reach age 72, which are referred to as Required Minimum Distributions (“RMDs”).

- Via required minimum distributions (RMDs).

- RMDs are the minimum amount you must withdraw each year from a retirement plan after reaching age 73. However, as is stated on the IRS website, Roth IRAs “do not require withdrawals until after the death of the owner.”***

- Via hardship distributions.

- Savers may be able to withdraw funds if they can show a substantial financial need. The IRS permits withdrawals for certain types of "substantial financial need," but generally this type of withdrawal is meant to cover medical expenses, funeral expenses, and similar emergencies. Unlike a loan, a hardship withdrawal does not need to be paid back.

- Via loans.

- A 401(k) loan is a way to borrow against your retirement account while agreeing to repay the balance, plus interest, within a specific timeframe. Loans generally have a term of 1-5 years, although your plan may allow a longer term if you use the loan to purchase a principal residence. Your loan must be repaid through payroll deductions or paid out in full through a lump sum payment.

- Savers can take out a "loan" from the vested balance of their plan. The IRS limits a loan amount to the greater of $50,000 or 50% of the saver's vested account balance. There may be restrictions in the plan, such as how many loans a single saver can have outstanding or how many loans a plan can have at any given time across all savers.

*This hypothetical scenario is for illustrative purposes only and is not intended to represent the performance of any specific investment. Past performance is not indicative of future results. Actual returns will vary and principal will fluctuate. Taxes are due on traditional contributions at the time of withdrawal. Performance for any investment is never guaranteed.

**Assumes a 7% growth rate, compounded monthly with each monthly payment occurring at the beginning of the period. Numbers have been rounded to the nearest thousand.

***There are exceptions to this rule for savers who own a certain percentage of the business.