Workplace Savings Programs

Helping employees save for retirement and beyond

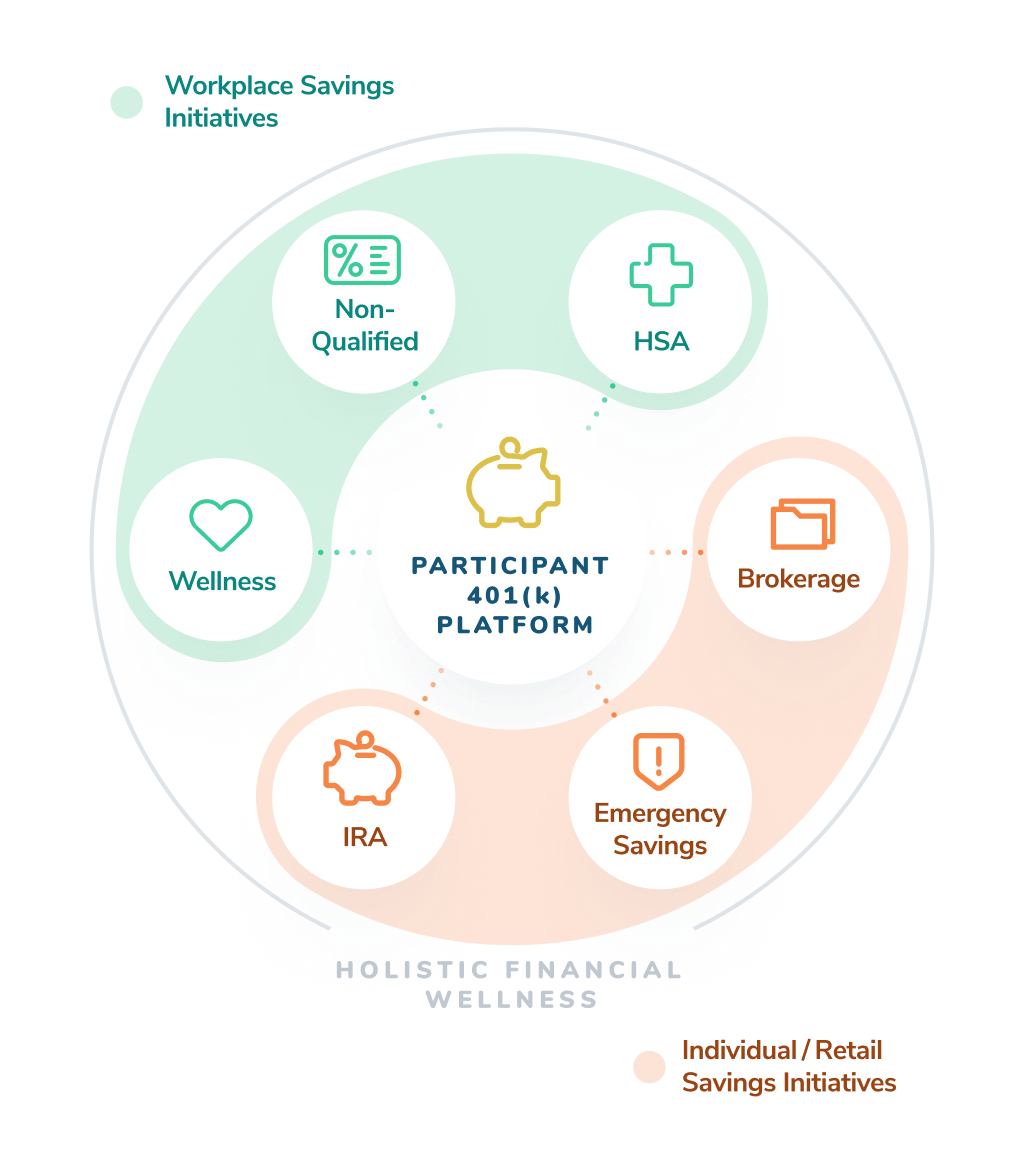

Powering the workplace savings ecosystem

The most powerful point of impact for long-term savings is at the paycheck, allowing for tax optimized investing. Vestwell provides the underlying infrastructure to power payroll deducted savings programs, starting with the 401(k) and moving into HSAs, IRAs, 529s, emergency funds, and more.

Beyond the 401(k)

Not everyone is an expert on the savings ecosystem, nor should they be. But having disparate accounts across various financial goals can be confusing for even the most well versed. Vestwell provides the infrastructure and data to help enable, initiate, and allocate funds across various savings vehicles.

Health Savings Account (HSA)

As one of the most tax advantageous investment options available, HSAs are an impactful way to help employees save for healthcare costs. Alongside 401(k)s, HSAs can be an especially important vehicle for significant later life expenses.

More about HSAs

A Health Savings Account (HSA) is a vehicle that helps individuals save for medical expenses while reducing their taxable income. They are only available to those enrolled in an "HSA-eligible" high-deductible health insurance plan as defined by the IRS. The biggest benefit of HSAs is that they are triple tax advantaged because you contribute to them pre-tax, you don't pay taxes on growth, and you also don't pay taxes on withdrawals. And because they can be invested, they can serve as another form of long-term investment, especially alongside a 401(k).

Individual Retirement Account (IRA)

When it comes to tax advantaged retirement plans, many individuals have IRAs in addition to their 401(k)s. But ensuring the two work hand in hand is important for creating a cohesive portfolio.

More about IRAs

An individual retirement account (IRA) allows individuals to save money for retirement while reducing their taxable income. Like 401(k)s, IRAs can be either traditional (tax-deferred) or Roth (after-tax). However, they have contribution limits (much lower than 401(k)s), penalties for early withdrawal, and required minimum distributions.

529

While saving for retirement can be critical to long-term security, many have pressing shorter-term needs as well. Configuring benefits to include advisor-led or direct tax-deductible 529 investments can provide better support for an individual's big-picture savings goals.

More about 529s

529s are tax-advantaged savings plans to help pay for education. They can be opened by anyone and must be assigned a beneficiary. 529s are run by the states so their rules on tax advantages differ by region. However, in all cases, the money grows on a tax-deferred basis, and as long as it's used for qualified education expenses, future withdrawals aren't subject to either state or federal taxes. As with most other long-term savings plans, non-qualified withdrawals are subject to penalty.

College Savings

Saving for a child’s education is a primary financial concern among parents, in addition to saving for retirement. Employers can help employees save for their children’s education by making direct contributions to employees’ 529 savings plans with the College SaveUp program.

More about College Savings

Families can use a tax-preferred 529 savings account to save for future education costs. There are two types of 529 plans: prepaid tuition plans and education savings plans. Through the College SaveUp program, employers can provide a benefit that helps employees contribute more to their education savings accounts.

Student Loan Repayment

Employees with student loan debt don’t have to sacrifice their retirement savings due to student loan repayment obligations. Student Loan Paydown is a workplace benefit that allows employers to make direct monthly contributions to employees’ student loans.

More about Student Loan Repayment

By contributing to employee student loans, employers can help their teams pay down their student loan debt faster and improve workforce engagement. Through this benefit, employers can help employees pay down debt faster, which can relieve stress and support overall financial wellness.

Emergency Savings

A 401(k) is not the same as a bank account. As such, having an emergency fund in addition to a retirement account is important. Not only does it protect from unexpected short-term financial needs, but it also helps retain the integrity of any long-term investments.

More about emergency savings

An emergency savings fund is an accessible safety net of cash or other liquid assets to use towards emergency expenses. Not only does it provide security for unexpected financial dilemmas, but it reduces the need to draw from a high-interest debt option like a credit card, or tap into a long-term investment like a retirement fund. Experts often recommend having three to six months' worth of expenses for times of need.