Savers

Vestwell when you need to save for what matters—whether it’s retirement, emergencies, education, or living with a disability, we meet you where you are. Our platform makes saving simple, accessible, and tailored to your financial journey.

What saving feels like.

Short, guided demos show how we turn complexity into clarity—giving every saver confidence from the start.

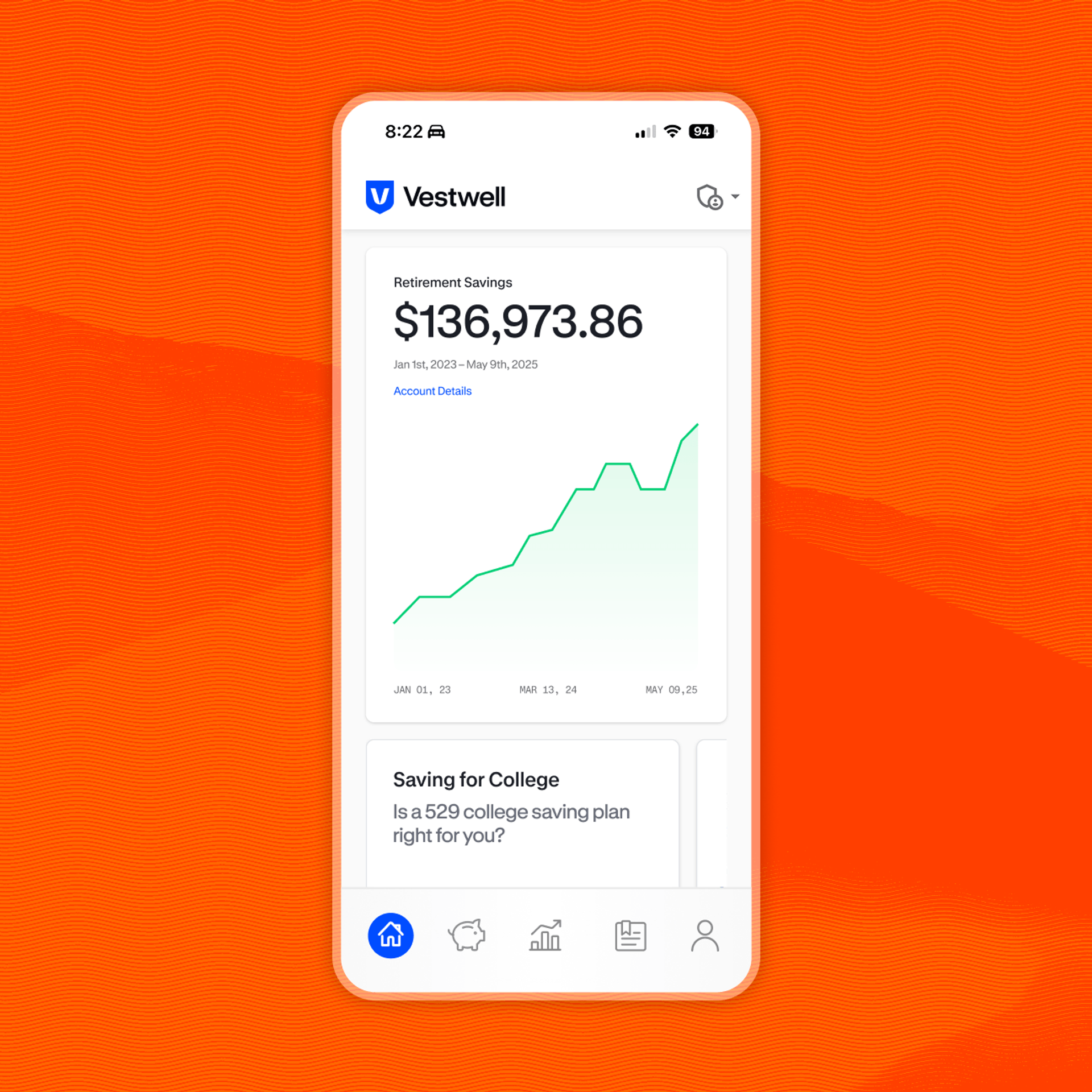

Monitor Account Growth & Performance

Informative graphics show the build up of your savings and your personal rate of return, keeping you informed and motivated to keep saving.

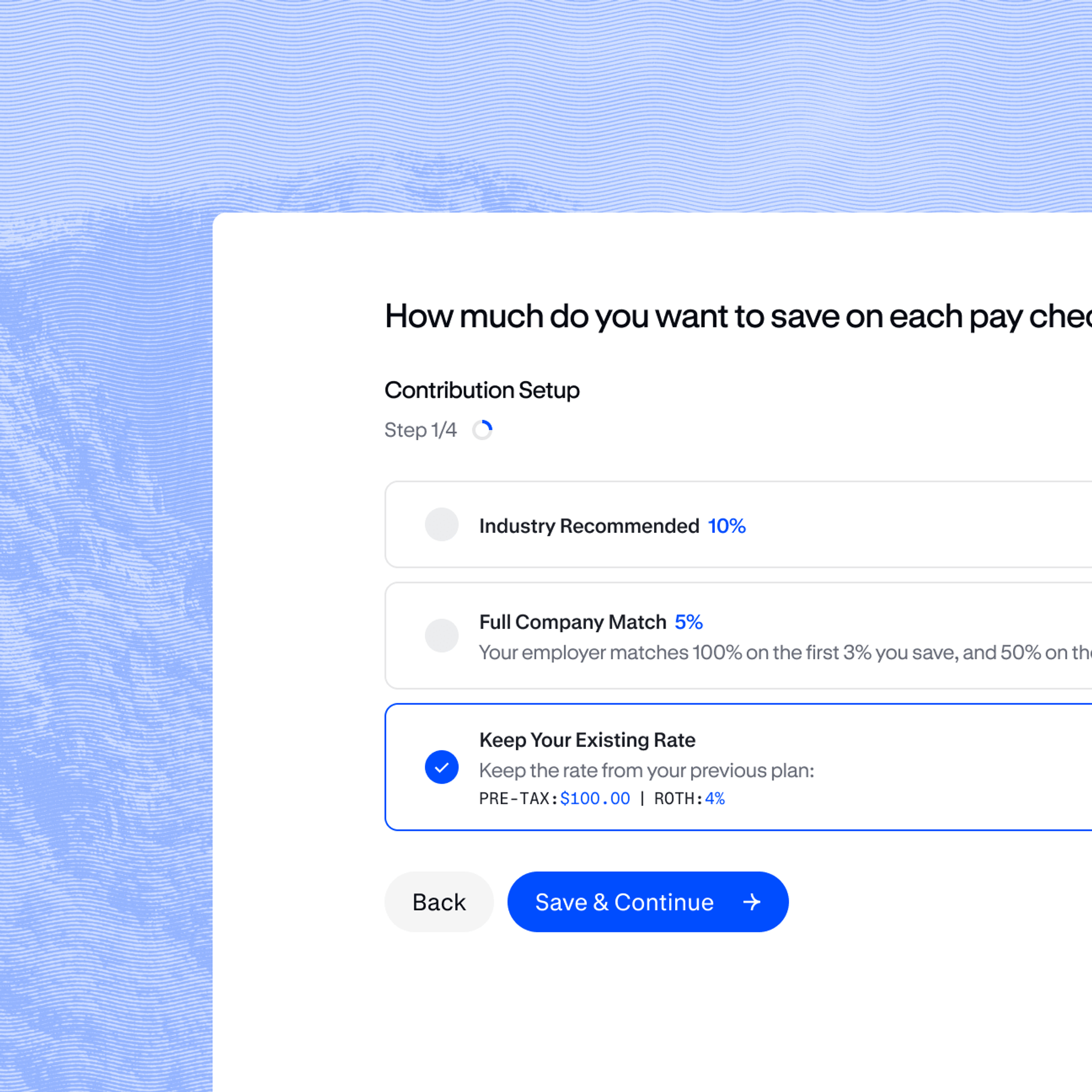

Manage How Your Money Is Invested

You direct where your money is invested via the investments offered within the plan. Follow simple workflows to reallocate your investments to fit your needs and goals.

Direct Money Into And Out Of Your Account With Ease

Whether it’s setting your savings rates or taking out a loan, it’s all done digitally via a simple UI. Rollover previous accounts with ease and track the status of all other transactions within a detailed account view.

Access Your Account From Anywhere Via Our Native Mobile App For iPhone And Android

Having your account in your hand is important, and you’ll have all the functionality present within the mobile app as you do on your desktop portal.

Mobile app

The modern savings platform in your pocket.

Growing businesses need benefits that keep pace with complexity. Vestwell helps mid-size teams streamline savings programs with flexible solutions, intuitive technology, and hands-on support. Whether you’re expanding acrossd locations or upgrading from a legacy provider, we make it easier to offer benefits that scale with your team.

Built to maximize your next dollar, backed by trust.

Vestwell for your next best dollar. Our platform gives you the confidence and tools to take control of your financial future before you get there. Seamlessly track and plan after retirement with a full picture of your savings in one place.

Enroll in Minutes

Set up your account quickly with a guided digital process.

Track Savings Anytime, Anywhere

Log in from your phone or desktop to view balances, check progress, and make changes on your terms.

Guided Every Step of the Way

In-app tips and helpful content ensure you understand your options as you save.

Here to help guide you every step of the way.

Start saving today.

Ready to start your savings journey? Log in or create an account to make saving a priority.

FAQ

Choosing a plan depends on your goals, your team, and where you are in your savings journey. Our team will guide you through plan design and highlight tax credits, employer match opportunities, and payroll integrations that make the most sense for you. With Vestwell, you don’t have to become an expert—we’ll walk you through the options and help you choose the path that’s right for your business or household.

Yes. If you already have savings with another provider, you can roll them into your Vestwell account without losing tax advantages or disrupting your progress. Our platform and support team make the process simple, so you can keep all your savings in one place and continue building toward your goals.

No. Accounts like ABLE or workplace savings are designed to help you save without jeopardizing key benefits. Vestwell partners with programs that protect your eligibility so you can grow your savings and maintain the support you need.

Yes. Contribution limits vary by account type (for example, retirement, 529 education, or ABLE savings), and many are set annually by the IRS or your state program. Our platform helps you track limits automatically so you can save confidently without over-contributing.

You can log in to your Vestwell account at any time to request a withdrawal. Depending on the type of account, you may have direct deposit, debit, or transfer options—making it simple to use your funds for qualified expenses or future goals.